Alert:

For more information on the cybersecurity incident, please visit the cybersecurity incident page.

The Canadian Securities Administrators (CSA) and the Investment Industry Regulatory Organization of Canada (IIROC and, together with the CSA, we) are publishing Joint Canadian Securities Administrators and Investment Industry Regulatory Organization of Canada Staff Notice 23-329 Short Selling in Canada (Notice) to provide an overview of the existing regulatory landscape surrounding short selling, give an update on current related initiatives and request public feedback on areas for regulatory consideration.

We believe that it is important and timely to review our regulatory framework to ensure it is current and appropriate given the way markets continue to evolve. This Notice reflects our commitment to do so, especially in light of public feedback we received with respect to short selling and international developments, described later in the Notice.

The CSA are also publishing today a summary of comments and responses to the CSA Consultation Paper 25-403 Activist Short Selling (Activist Short Selling Consultation Paper).1The Activist Short Selling Consultation Paper was published on December 3, 2020. Its purpose was to facilitate the discussion of concerns relating to activist short selling and its potential impact on capital markets. Some of the comments received in response to the Activist Short Selling Consultation Paper addressed topics broader than activist short selling activities and related to short selling and short selling regulation in general. Similar issues have also been raised by other stakeholders. These comments are summarized in the summary and responses to the Activist Short Selling Consultation Paper and published today in CSA Staff Notice 25-306 Activist Short Selling Update (Staff Notice 25-306). We discuss the broader comments related to short selling in this Notice.

While this Notice does not directly cover the Canadian trade settlement regime, we also discuss, at a high level, failed trades and related initiatives, to provide additional context to the extent that they may relate to short selling.

The Notice is organized as follows:

IIROC’s Universal Market Integrity Rules (UMIR) define a “short sale”2 as a sale of a security, other than a derivative instrument, which the seller does not own either directly or through an agent or trustee.3It involves selling securities at the current market price either with the expectation of being able to cover the short position by purchasing later at a lower price, thus making a profit, or to lock in a profit arising from a difference in price between the securities sold short and a related security. Short selling is a legitimate trading practice that helps market participants manage risk, contributes to market liquidity and promotes price discovery.

Short selling carries certain risks. For example, a short seller may incur potentially unlimited costs to close the short position if the price of the particular security rises.

The term "failed trade" is not defined in securities legislation. However, a failed trade is generally understood to occur when a seller (whether short or long) fails to deliver securities or the buyer fails to pay the funds when delivery/payment is due, currently on the second business day after the trade date, unless a later settlement date is agreed to by all parties at the time of the trade. Failed trades may also occur when there are issues with instructions of the buyer and the seller regarding settlement (for example, when there are different instructions from the buyer and the seller, or one party of the trade has not provided instructions or provided them too late). In the context of this Notice, “failed trades”, “settlement fails or failures” and “fail to deliver”, all mean failure to deliver securities on the settlement date.

UMIR Rule 1.1 defines “failed trade.”4It includes a short sale by an account that has failed to make available the securities for settlement or has failed to make arrangements with a Participant or Access Person (as defined in UMIR)5to borrow the securities in time to deliver on the settlement date.

Short selling is subject to a well-developed framework comprising Canadian securities legislation and IIROC requirements and is mostly overseen by IIROC. This framework includes a detailed reporting regime that provides IIROC with timely information which IIROC uses to monitor and supervise potentially inappropriate short selling practices.

Canadian securities legislation requires a person who places an order for the sale of a security with a registered dealer to declare to the dealer at the time of placing the order if they do not own the security.6

Securities legislation7 and National Instrument 23-101 Trading Rules8 (NI 23-101) prohibit activities that are manipulative and/or deceptive, which could occur in connection with short selling.

IIROC has several requirements relevant to short selling applicable to Participants9 or Access Persons10including:

UMIR also requires Participants and Access Persons to calculate and report to IIROC the aggregate short positions of each individual account twice a month.16 IIROC consolidates and publishes a Consolidated Short Position Report showing the aggregate short positions on all listed securities as of the current reporting date and the net change in short positions from the previous reporting date, on a per security basis, on its website.17IIROC also aggregates trades marked “short sale” from all marketplaces it monitors, consolidates that information, and publishes a semi-monthly report showing the total industry short sales for each security over the reporting period.18

Like securities legislation, UMIR also prohibits activities that are manipulative and/or deceptive. In the context of short selling, these include entering an order for the sale of a security without, at the time of entering the order, having a reasonable expectation of settling any trade that would result from the execution of the order on the settlement date. As such, short selling without having a reasonable expectation to settle the resulting trades on settlement date, generally two days after trade date, is not permitted under UMIR. 19

On August 17, 2022, IIROC issued guidance confirming the existing obligation of a Participant to have a reasonable expectation to settle a resulting trade on the settlement date, rather than having the expectation to settle the trade on some future date, such as the date securities owned by the seller that are subject to resale restriction become freely tradeable.20

IIROC also monitors for potentially abusive trading activity. In the context of short selling activity, IIROC uses algorithms to monitor for unusual levels of short selling coupled with significant price movements and reviews alerts to determine the cause of the price movement and whether there is an indication of abusive trading activities. IIROC may also review social media or chatrooms as well as Extended Failed Trades reports for indications of settlement issues.

IIROC has additional alerts that detect changes in the historical pattern of short selling for a particular security. These alerts allow IIROC to determine if short selling is becoming concentrated within a particular dealer or client. If unusual levels of short selling are detected, IIROC can:

If appropriate, IIROC may also refer the matter to the enforcement branch of the appropriate CSA jurisdiction for additional investigation and action.

As noted above, IIROC requires Participants to mark all orders representing a short sale as either “short” or “short-marking exempt”. This is part of a broader requirement in UMIR that Participants use the correct identifier or designation on an order sent to a marketplace regulated by IIROC.21Where there is a missing or erroneous marker or identifier on the order and that order has been executed at least in part, the Participant is required to file a report to the Regulatory Marker Correction System.22IIROC reviews its Participants’ use of order markers during compliance reviews.

IIROC recently completed a study of failed trades. The study was based on five years (April 1, 2015 – March 31, 2020) of settlement data from the CDS Clearing and Depository Services Inc. (CDS) related to continuous net settlement (CNS),23 outstanding positions, buy-ins and trade-for-trade (TFT)24 settlement transactions. IIROC Notice 22-0190 includes the results of IIROC’s study and additional discussion of the CNS and TFT processes. In essence, the study identified several considerations:

At Appendix A, we have included a detailed history of IIROC’s short selling requirements, a summary of studies that have been conducted over time to assess their continuing adequacy and the rationale supporting why such requirements continue to be included or have been removed.

It is widely acknowledged that short selling plays an important role in the financial markets by promoting transparency and contributing to liquidity and price discovery, and thus contributing to market integrity and investor protection. Short selling can also be a legitimate investment management strategy used for mitigating portfolio risk by hedging short positions against long positions, so that losses are mitigated regardless of the direction of the market.

Short sellers, particularly activist short sellers who publicly announce that they have a short position in a security, may provide new information about issuers that can assist in ensuring the price of their securities is more reflective of their underlying value. For example, short sellers identify securities they think could be overvalued. Often, after disclosure by activist short sellers, a correction occurs in the market price of these securities. As we described in the Activist Short Selling Consultation Paper, sometimes issuers pursue certain actions in response to short selling campaigns which may include a change in management or hiring a new auditor or private investigator.

However, short selling is not without controversy and some stakeholders hold negative perceptions about short selling or certain aspects of short selling activities. A common theme of concerns expressed is that issuers perceive the Canadian regulatory regime as lax compared to other jurisdictions, especially the U.S., which makes it easier to conduct an activist campaign that unfairly targets Canadian issuers.

As we indicated in the past, and explain in further detail in Appendix A, we believe that Canada’s regulatory regime governing short sales is generally consistent with the four principles for the effective regulation of short selling published by the International Organization of Securities Commissions (IOSCO) in 2009.26Further, as we concluded in Staff Notice 25-306, we have not received evidence of specific issues arising from activist short selling campaigns that would justify a regulatory response. That said, we acknowledge the comments surrounding short selling in general, some of which have been raised more recently. We discuss the key themes below and invite further feedback from the public.

The “tick test” was a restriction on the price at which certain types of trades can occur. In the case of short sales subject to the tick test, the sale could not occur at a lower price than the previous trade, subject to limited exceptions.

As explained in more detail in Appendix A, IIROC amended UMIR in March 2012 to repeal the tick test. This was supported by empirical evidence from short sales and failed trade studies in the Canadian market. These studies did not find a relationship between rapid price declines and unusual short selling activity and did not support adopting an alternative uptick rule similar to Rule 201 of the U.S. Securities and Exchange Commission (SEC).28

Concerns have been expressed regarding a perceived negative impact that resulted from the repeal of the tick test. Several commenters that provided responses to the Activist Short Selling Consultation Paper recommended that the CSA review the impact that the removal of the tick test has had on the market.

IIROC monitors the proportion of short selling relative to total sales, and the frequency of short sales that are executed on a downtick. Some results of this monitoring are included as Appendix C. These results show that:

Concerns have been raised that market participants may engage in short selling where they enter short sale orders without an intention to settle the resulting trades on settlement date, purely as a means to drive down the price of an issuer’s securities. The short seller fails to deliver the shares on the settlement date and anticipates settling the trade when the securities can be bought at a later date in the open market at a price that is profitable to the seller.

As noted above, there are existing requirements in Canadian securities legislation and UMIR that prohibit manipulative and deceptive activities. UMIR specifies that entering an order to sell a security without having a reasonable expectation of settling the resulting trade on settlement date is considered a false or misleading appearance of trading activity and thus a manipulative and deceptive activity.29

As noted earlier, IIROC published guidance on August 17, 2022 clarifying that Participants, before entering a short sale order, must have a reasonable expectation that they have or will have sufficient securities to allow the Participant to settle any resulting trade on the settlement date for that trade.30In this notice, IIROC provides examples where a Participant would not be able to demonstrate a reasonable expectation that sufficient shares would be available on settlement date and the entry of the order would be prohibited.

In addition, as described above, IIROC has certain “pre-borrow” requirements that apply, including the restriction on Participants or Access Persons from making further short sales where an Extended Failed Trade report that relates to a sale of a security failing to settle was filed with IIROC. Specifically, further short sales generally cannot be made by that Participant (acting as principal or as agent) or by an Access Person without prior arrangements to borrow the securities necessary for settlement.31 Participants and Access Persons must also make prior arrangements to borrow any security designated by IIROC as a “Pre-Borrow Security” before entering an order to sell short on a marketplace.32

Despite these requirements, views were expressed in response to the Activist Short Selling Consultation Paper that the current requirements in Canada are not stringent enough, especially when compared with those in the U.S. Some stakeholders noted that in the U.S, Regulation SHO requires a broker-dealer to not accept a short sale order in an equity security unless it has (i) borrowed the security or entered into a bona-fide arrangement to borrow the security; or (ii) reasonable grounds to believe that the security can be borrowed so that it can be delivered on the date delivery is due; and (iii) documented compliance with this requirement.33

In Ontario, the Ontario Capital Markets Modernization Taskforce (CMM Taskforce) recommended that IIROC revise UMIR to require a Participant to confirm the ability to borrow securities prior to accepting a short sale order from another person or entering an order for its own account.34

We ask whether the market has changed to support the introduction of such requirements at this time. In particular, we have the following questions:

Questions:

We have discussed above IIROC’s requirements for Participants and Access Persons to report Extended Failed Trades. IIROC also has an anti-avoidance provision to prohibit Participants from entering into a transaction or series of transactions in an attempt to “re-age” the default in order to avoid filing an Extended Failed Trade Report, which would be a violation of the requirement in UMIR 2.1 to trade openly and fairly.35

The failed trade is not reportable until ten trading days following the settlement date. This was to allow for administrative delays that may impact settlement and to better identify those transactions of greater concern.

Some concerns have been raised by stakeholders about the ten-trading day threshold. The concern is that this timeline is too long for an unsettled trade to be reported and should be shortened.

Questions:

We described above how IIROC publicly discloses short positions by publishing the Consolidated Short Position Report twice monthly. In contrast to other jurisdictions (such as the European Union and Australia), there are no regulatory or public reporting requirements or obligations to disclose information on the short position of an individual account. Even so, it is not uncommon for an activist short seller to voluntarily disclose that they are short a particular security when they commence a campaign.

As described in Appendix A, IIROC has conducted extensive consultations on transparency measures that would provide timely information to the market. The Short Sale Trading Statistics Summary Report36 was introduced in 2013, and in 2016, following additional consultation, IIROC also started publishing the Consolidated Short Position Report37, also described in Appendix A. IIROC also publishes the Short Sale Trading Corrections Report38 twice a month. This report aggregates trade marker corrections affecting short sale traded volume submitted through the Regulatory Marker Correction System.

Comments provided in response to the Activist Short Selling Consultation Paper supporting additional transparency are summarized in Staff Notice 25-306 published today and include recommendations to require the reporting of the identity of short sellers and short positions to the regulator, the public or both. Other comments cautioned that additional transparency could have unintended consequences, such as promoting group behaviour that would drive down a target issuer’s stock price.

We are reviewing international initiatives to enhance reporting and disclosure requirements, such as those described in Appendix B of this Notice.

Questions:

In Canada, eligible debt and equity securities are cleared and deposited through CDSX, the clearing and settlement system of the CDS. CDSX has a Continuous Net Settlement Service (CNS), which is designed to clear and settle primarily equity trades transacted on a Canadian marketplace.

Within CNS, a “buy-in” process enables a buyer in a transaction to accelerate the settlement of outstanding, unsettled CNS positions from its seller(s) which are identified in CDS procedures as “to-receive”. Outstanding to-receive CNS positions are those quantities of shares which have failed to settle on the “value date” (the date on which the parties to a trade have agreed that it is to be settled). The buy-in process is initiated when a buyer (i.e. receiver) chooses to enter an “intent to buy-in” outstanding to-receive positions in CDSX against an outstanding quantity of shares owed to them. The participant owing the specified security is provided with a 48-hour notice that they may be held liable to deliver on some or all of their portion of the buy-in security.

The CMM Taskforce, in its Final Report,39 noted that, in contrast with the U.S.40and the European Union41, there are no mandatory close-out or buy-in provisions in Canada. The CMM Taskforce recommended that, should a short sale fail to settle, the short seller be subject to a mandatory buy-in. To allow for fails due to administrative issues, the buy-in requirement would be triggered at settlement date +2 days. The CMM Taskforce recommended that the obligation to execute the buy-in rest with the investment dealer and that exemptions be considered for additional activities that may cause a legitimate settlement delay.

Question

Conclusion

As we noted in the past, we are of the view that Canada’s regulatory regime governing short sales is generally consistent with the four IOSCO principles for the effective regulation of short selling. However, we are aware of the comments raised by various stakeholders, including the expression of a number of concerns. In this Notice, we seek input on the items discussed above. In addition to answers to the questions set out above, we also seek general comment on other aspects of short selling where stakeholders believe there is room for regulatory initiatives.

Please submit your comments in writing, on or before March 8, 2023. Please send your comments in writing to the following addresses:

The Investment Industry Regulatory Organization of Canada

Attn: Kevin McCoy Vice-President, Market Compliance and Policy

121 King Street West Suite 2000, Toronto, Ontario, M5H 3T9

Email: kmccoy@iiroc.ca

and

The Secretary

Ontario Securities Commission

20 Queen Street West, 22nd floor, Toronto, Ontario M5H 3S8

comments@osc.gov.on.ca

and

Me Philippe Lebel

Secrétaire et directeur général des affaires juridiques

Autorité des marchés financiers

Place de la Cité, tour Cominar

2640, boulevard Laurier, bureau 400

Québec (Québec) G1V 5C1

Télécopieur : 514 864-63811

consultation-en-cours@lautorite.qc.ca

Please refer your questions to any of the following CSA and IIROC staff:

| Timothy Baikie Senior Legal Counsel, Market Regulation Ontario Securities Commission tbaikie@osc.gov.on.ca | Hanna Cho Legal Counsel, Market Regulation Ontario Securities Commission hcho@osc.gov.on.ca |

| Ruxandra Smith Senior Accountant, Market Regulation Ontario Securities Commission ruxsmith@osc.gov.on.ca | Serge Boisvert Senior Policy Advisor Autorité des marchés financiers Serge.boisvert@lautorite.qc.ca |

| Roland Geiling Derivatives Analyst Autorité des marchés financiers Roland.geiling@lautorite.qc.ca | Jesse Ahlan Regulatory Analyst, Market Structure Alberta Securities Commission Jesse.ahlan@asc.ca |

| Michael Grecoff Securities Market Specialist British Columbia Securities Commission mgrecoff@bcsc.bc.ca | H. Zach Masum Manager, Legal Services British Columbia Securities Commission zmasum@bcsc.bc.ca |

| Tyler Ritchie Investigator Manitoba Securities Commission Tyler.Ritchie@gov.mb.ca | Doug Harris General Counsel, Director of Market Regulation and Policy and Secretary Nova Scotia Securities Commission doug.harris@novascotia.ca |

| Theodora Lam Senior Policy Counsel, Market Regulation Policy Investment Industry Regulatory Organization of Canada tlam@iiroc.ca | Kevin McCoy Vice-President, Market Compliance and Policy Investment Industry Regulatory Organization of Canada kmccoy@iiroc.ca |

There has been a steady evolution of short selling regulation in Canada. Beginning in 2002, Market Regulation Services Inc. (RS), a predecessor organization to IIROC, imposed UMIR requirements on Participants42 to:

These requirements reflected short selling rules already in place on exchanges that retained RS to act as regulation services provider.

In the following years, IIROC expanded on these requirements and, among other things44, provided specific exemptions45 from the tick test, consistent with IOSCO’s Principles of Short Sale Regulation.46

To ensure the overall effectiveness of regulation of equity trading in Canada, IIROC took the following steps which culminated in the 2008 amendments to UMIR:

IIROC launched a strategic review that included looking at the short selling regime in UMIR47 by:

RS and the Investment Dealers Association (IDA), both IIROC’s precursors, the CSA and staff from CDS, TSX and the Bourse de Montréal, looked at short selling further and formed a working group on Short Selling and Failed Trade Issues (Working Group). 49 This Working Group monitored regulatory developments in the U.S. including the 2004 SEC SHO Pilot Project50 which evaluated the effectiveness and necessity of price restrictions (tick test) in short selling. The Working Group also looked at data on failed trades from November 2004 to February 2005 and found the market value of fails in the issues on the “fail list”51 using the U.S. criteria would account for approximately 12.2% of the market value of all failed trades.52

As a result of this work, IIROC questioned whether the benefits of a US-style “fail list” for Canadian markets in 2007 would be commensurate with the costs due to:

To get data on the prevalence of failed trades, including on the contribution of short sales in the occurrence of failed trades, IIROC conducted a statistical study of failed trades on Canadian marketplaces and published its findings in April 2007 (2007 Failed Trade Study). The 2007 Failed Trade Study results showed that a short sale had a lower probability of failing than trades generally and that the principal reason for trade failures was administrative error. At the time, IIROC concluded that the concepts of short sale regulation and failed trade regulation were distinct and that the measures adopted to address failed trades should be broad enough to encourage timely settlement of trades in all circumstances. As a result, IIROC recommended looking further into:

As part of IIROC’s ongoing commitment to monitor trading activity on equity marketplaces in Canada to ensure that its rules for market integrity are informed by relevant and timely data, IIROC completed a study of trends in trading activity, short selling and failed trades (2008 Trends Study) and published its report in February 2009. The 2008 Trends Study indicated, among other findings, that:

Findings from the 2008 Trends Study did not support the need in Canada to follow actions on short selling taken at the time by the SEC, including the Regulation SHO proposal.55

Results from the body of work described above led to IIROC’s decision to amend UMIR with respect to short selling and failed trades in 2008 (2008 UMIR Amendments), which included:

IIROC amended UMIR to provide for the ability to prohibit short selling in particular securities or class of securities in real-time (Short Sale Ineligible Security56) and respond to developments in trading where rates of failed trades had become excessive.57

IIROC also clarified requirements that must be met for a seller to be considered the owner of securities at the time of a sale, including that if a seller has not taken all necessary steps to become legally entitled to the security, the seller would be considered to be making a short sale and the order must be identified accordingly.58

IIROC required Participants and Access Persons to report “failed trades” where the failure was not resolved within ten trading days following the original settlement date of the trade (EFTR).59 IIROC also implemented a new web-based reporting system for EFTRs to identify “problem” fails so that IIROC would be able to assess the reasons for the failure and monitor the steps taken to resolve the problem.60 IIROC also included an anti-avoidance provision to prohibit Participants and Access Persons from entering into a transaction or series of transactions in an attempt to “re-age” the default in order to avoid filing an EFTR, which would be a violation of the requirement to trade openly and fairly in UMIR 2.1.

IIROC prohibited the cancellation or variation61 of a trade unless the variation or cancellation was made by IIROC or with notice to IIROC (TVCR).62 TVCR reports allowed IIROC to review these changes and ensure that the variation or cancellation is for a bona fide reason and not part of a manipulative or deceptive manner of trading.63

IIROC continued to monitor short selling and failed trades and enhanced its surveillance regime to see if further regulatory action would be required. The following measures adopted by IIROC and further studies ultimately led to further amendments in UMIR in 2012:

IIROC introduced additional alerts that detected changes in the historic pattern of short selling for a particular security. These alerts allowed IIROC to determine if short selling was becoming concentrated within particular dealers or clients.64 If unusual levels of short selling were detected, IIROC would also have the ability to:

IIROC continued to monitor against regulatory arbitrage opportunities by undertaking a study (Short Prohibition Study) to evaluate the impact of the CSA orders 67(Orders), which prohibited short sales of certain financial issuers listed on the TSX that were also listed on an exchange in the U.S. (Restricted Financials). These temporary orders were issued by CSA jurisdictions as a precautionary measure to prevent regulatory arbitrage with respect to short selling of inter-listed financial sector issuers because of initiatives taken by the Securities and Exchange Commission to prohibit short selling of financial sector issuers.

The Short Prohibition Study compared rates of trade failure of Restricted Financials to those of other issuers in the financial sector that were only listed on the TSX (Non-Restricted Financials). The analysis covered the periods before, during, and after the Orders were in effect68. IIROC published its findings in February 2009 which indicated the issuance of the Orders:

To see if short selling activity was the cause or a contributing factor to significant price declines, IIROC conducted and published a multi-year study (2011 TSXV Study) on the relationship between price movement and short sale activity on the TSXV during May 1, 2007 to April 30, 2010, when trading on the TSXV was subject to price restrictions on short sales70. IIROC found that the prices and rates of short selling activity tended to move in tandem and that, in periods of most significant price decline, “shorts” were in the market buying securities to cover their positions thereby providing price support.71 The data from the 2011 TSXV Study also suggested that:72

IIROC also updated its 2008 Trends Study by publishing a multi-year study on trends in trading activity, short sales and failed trades for the period May 1, 2007 to April 30, 2010 (2011 Trends Study). The 2011 Trends Study found that the rates of short sales were relatively constant throughout the period and that rates of trade failure generally declined. Taken together with IIROC’s previous empirical studies, IIROC found that the Canadian market did not experience problems with short selling, particularly naked short sales and failed trades that may have been evident in other jurisdictions.

To determine whether IIROC should consider similar short sale circuit breaker requirements as the SEC at the time, IIROC monitored and reviewed short selling activity on Canadian marketplaces from February 28 to April 29, 2011 in inter-listed securities where a short sale circuit breaker had been triggered in the U.S. Based on IIROC’s empirical studies, IIROC did not find a relationship between rapid price declines and unusual short selling activity, and did not find there was evidence of a systemic migration of short selling activity of inter-listed securities to Canadian markets when short sale circuit breakers were in effect in the U.S. Based on this study, IIROC concluded that Canada did not need to adopt the same short sale circuit breaker system and alternative uptick rules similar to the SEC’s Rule 201.75

Supported by the empirical evidence from the above studies on short sales and failed trades in the Canadian market, IIROC amended UMIR in March 2012 to repeal the tick test (2012 UMIR Amendments).76 This amendment paralleled the SEC’s repeal of price restrictions on short sales that became effective on July 7, 2007, following a multi-year “pilot project” which concluded that price restrictions had no effect on market prices.77 Before the 2012 UMIR Amendments, IIROC had to provide an exemption from the price restrictions on short sales with respect to securities that were inter-listed on an exchange in the U.S.78

Based on IIROC’s studies, IIROC believed there were better mechanisms than the tick test to detect and address abusive short selling,79 and implemented the following new initiatives on short selling and failed trades as part of the 2012 UMIR Amendments:

While short selling with no reasonable expectation to settle on settlement date was already prohibited as a type of manipulative and deceptive activity under UMIR 2.280, IIROC introduced the following limited pre-borrow requirements in March 2012 that would apply even if there was a reasonable expectation to settle:81 Participants or Access Persons must make arrangements to borrow the securities necessary for settlement before entering an order for a short sale on a marketplace for a security which has been designated by IIROC as a “Pre-Borrow Security”, or where a Participant has filed an EFTR at any time in the past with respect to:

IIROC also took additional steps to enhance its monitoring of short selling by introducing a new short-marking exempt marker82, which by identifying trading that is directionally neutral and has a horizon of a day or less, increased IIROC’s ability to monitor selling that takes a directional position.

While the CSA and IIROC believed that the regulatory framework following the 2012 UMIR Amendments governing short selling and failed trades in Canada was generally consistent with IOSCO principles, on March 2, 2012, the CSA and IIROC issued a consultation paper on approaches to transparency of short sales and short positions.83 The purpose of this consultation paper was to:

There was no clear consensus among the commenters who responded to the consultation paper that specific improvements were needed; the majority of respondents believed that the current requirements in UMIR, including the 2012 UMIR Amendments, were adequate. The working group concluded that additional measures were not needed or desirable at that time but monitoring of domestic and international developments should continue.84

As part of IIROC’s overall strategy on the regulation of short selling and failed trades, IIROC believes in providing greater transparency regarding short selling in a way that would provide timely information to the market. As a result, IIROC began publishing the Short Sale Trading Summary Report in 2013 on its website on a semi-monthly basis.85 This report sets out the proportion of short sales in the total trading activity of each listed security across all equity marketplaces for each period.86 While no one data source can provide a “complete” picture of short sale activity or positions, these semi-monthly trading summaries provided timely information in a cost efficient manner and supplemented the information available through the semi-monthly short position reports.87

To further understand and explore issues affecting small-cap issuers, IIROC hosted roundtables in 201488 and 201689. In order to facilitate discussions at the 2014 roundtable, IIROC reviewed trading data during January 1, 2012 to March 31, 2014 and found that:

As part of the response to the discussions at the 2016 roundtable, IIROC:

In Europe, existing disclosure requirements are under review. Specifically, the European Securities and Market Authority (ESMA) recently published a Consultation Paper – Review of certain aspects of the Short Selling Regulation91in which, among other things, they seek comment on the existing framework for transparency and publication of net short positions. ESMA published its final report to the European Commission on March 22, 2022. This final report proposed amendments to improve ESMA’s operation, focused on clarifying the procedures for the issuance of short and long-term bans, ESMA’s intervention powers and proposes to enhance its rules against uncovered short sales by introducing record keeping requirements and harmonization of sanctions. It also includes a review of the framework for transparency and the publication of net short position reports.92

In the U.S., the Financial Industry Regulatory Authority (FINRA) published a request for comment on potential enhancements to its short selling program, which would include modifications to its short interest reporting requirements.93 The public comment period, initially set at August 4, 2021, was extended to September 30, 2021. If implemented, such changes would change the frequency and content of information reported to FINRA and the information that would be made publicly available.

Also in the U.S., on November 18, 2021, the SEC published for a 30-day comment period proposed new Exchange Act Rule 10c-1 (proposed Rule 10c-1), which would increase transparency of securities lending transactions. The proposal is to require lenders of securities to provide the material terms of securities lending transactions to a registered national securities association, such as FINRA. FINRA would make some of the information available to the public.94 On February 25, 2022, the SEC indicated that it reopened the comment period for this proposed Rule 10c-1. The comment period for this proposal ended on April 1, 2022.

On February 25, 2022, the SEC proposed new Exchange Act Rule 13f-2 (proposed Rule 13f-2)95 and amendments to Regulation SHO and to the national market system plan governing the consolidated audit trail to increase market transparency regarding short selling. The proposed Rule 13f-2 and Form SHO would require that institutional money managers file on the SEC’s EDGAR system, on a monthly basis, certain short sale related data, some of which would be aggregated and made public. The proposed Form SHO would be filed within 14 calendar days after the end of each calendar month for equity securities that exceed certain thresholds. Such information would include the name of the security, end of month gross short position and daily trading activity that affects a manager’s reported gross short position for each settlement date during the calendar month reporting period. The SEC would publish certain information for the securities, including the aggregated gross short position across all reporting institutional money managers. The extended comment period for proposed Rule 13f-2 ended on April 26, 2022.

***The vertical line indicates when the tick restrictions were removed***

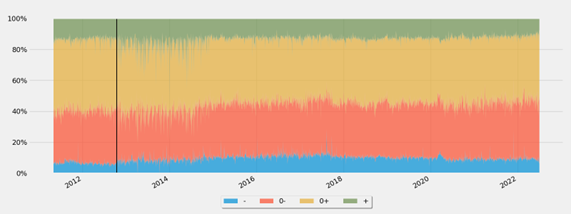

Fig 1 - Short Sale Volume Composition by Market Ticks - TSX, All Securities

Fig 1 shows the short sale volume composition by market ticks for TSX listed securities. The percentage of short sales of TSX listed securities executed on a down-tick was about 10% between 2012 - 2022. This was only slightly higher than prior to the repeal of the tick-test.

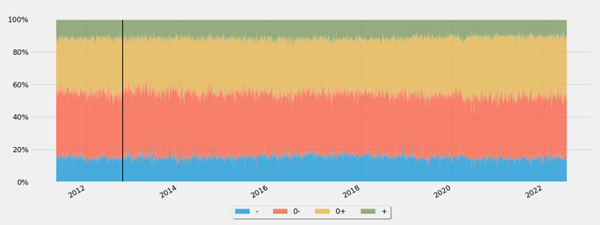

Fig 2 – Long Sale (excluding SME) Volume Composition by Market Ticks - TSX, All Securities

Fig 2 shows the long sale (excluding SME) volume composition by market ticks for TSX listed securities. The percentage of TSX listed securities long sales executed on a down-tick was about 15% between 2012 - 2022.

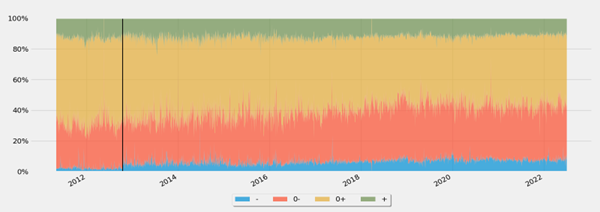

Fig 3 - Short Sale Volume Composition by Market Ticks - TSXV, All Securities

Fig 3 shows the short sale volume composition by market ticks for TSXV listed securities. The percentage of short sales of TSXV listed securities executed on a down-tick was about 8% between 2012 - 2022. This was higher than prior to the repeal of the tick-test.

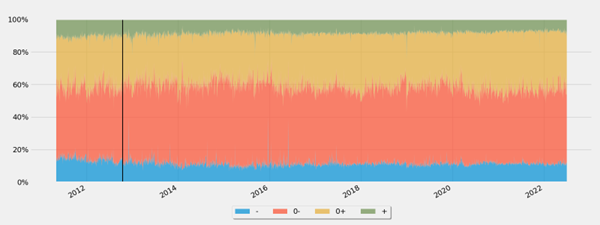

Fig 4. - Long Sale (excluding SME) Volume Composition by Market Ticks - TSXV, All Securities

Fig 4 shows the long sale (excluding SME) volume composition by market ticks for TSXV listed securities. The percentage of TSXV listed securities long sales executed on a down-tick was about 12% between 2012 - 2022.

**The TSX and TSXV data is provided as a proxy for marketplaces that list junior securities and marketplaces that list senior securities. At the time the tick restriction was moved CSE had limited listings and market activity and NEO had not yet launched. As a result the data from both CSE and NEO was less informative.**

12/08/22

22-0189

Welcome to CIRO.ca!

You can find the Canadian Investment Regulatory Organization (CIRO) at CIRO.ca with our fresh look and feel.