Alert:

For more information on the cybersecurity incident, please visit the cybersecurity incident page.

The know-your-client (“KYC”) process is one of the most fundamental obligations under securities legislation and one of the most important elements of investor protection. Some MFDA Members have implemented investor questionnaires to help address the challenges in the KYC process. Many other Members have expressed interest in implementing a questionnaire approach in the future.

To provide additional guidance in this area to MFDA Members, the MFDA has developed a Discussion Paper on the use of investor questionnaires (titled “Improving the Know Your Client Process”). The Discussion Paper includes a Sample Investor Questionnaire attached as Appendix “A”. Use of these materials is not mandatory. As noted, they are being provided as guidance to support those Members who wish to use questionnaires as part of their process for collecting KYC information. The MFDA will also be issuing a webcast for Members on the Discussion Paper and Sample Questionnaire.

Members who would like to implement a questionnaire in their KYC process, including the Sample Questionnaire provided in the Discussion Paper, are encouraged to discuss their plans with their respective Compliance Manager prior to implementation.

The know-your-client (“KYC”) process is one of the most fundamental obligations under securities legislation and one of the most important elements of investor protection. However, the process can be challenging for both clients and Approved Persons. Investors may not always understand the industry terminology used on KYC forms and research reveals that many investors do not understand the relationship between risk and return.1,2 Approved Persons face the challenge of trying to engage clients in the KYC process while recognizing that clients may have significantly different backgrounds, levels of education and degrees of openness when it comes to discussing their personal financial situation and attitude towards risk.

Some Members have implemented investor profile or risk profile questionnaires (“investor questionnaires”) to help address the challenges in the KYC process, and many other Members have expressed interest in implementing a questionnaire approach in the future. In addition, several mutual fund companies provide questionnaires that are used for their investment portfolio solutions.

Measuring risk tolerance is complex and as a result risk profiling is not an exact science. Nonetheless, a well-designed questionnaire can still make an important contribution to the KYC process. When investor questionnaires are used properly within the KYC and suitability process they can help to provide structure, promote consistency and support the discussion a client has with their Approved Person regarding their investment needs, capacity to withstand losses and attitude towards risk.

The use of a questionnaire or similar tool is only part of the full KYC process and just the beginning of a thorough conversation between the client and the Approved Person. A questionnaire can be an excellent starting point for deeper discussions around client goals, product risks and realistic investment return expectations. This is where the experience and knowledge of an Approved Person can add real value for clients.

The objectives of this paper are to share MFDA staff observations on a topic of interest to many Members and encourage discussion and consideration of how investor questionnaires can be used to improve the KYC process for investors, Approved Persons and Members.

While the structure, questions and scoring used in specific questionnaires differs, there are several general principles that are observed in any well-designed questionnaire. An effective investor questionnaire and accompanying process should:

Questions included in investor questionnaires can be broadly classified into certain types:

The first three types of questions help to measure the investor’s willingness to incur risk (risk attitude) while the next three types help to measure the investor’s ability or capacity to withstand risk (risk capacity).3 The investor’s willingness to accept risk is more subjective and is affected by an investor’s past experiences and understanding of financial risks and risk/ return trade-offs. In contrast, risk capacity looks at how much risk an investor can afford to take which can be measured more objectively, taking into account factors such as the investor’s income and net worth. Risk attitude and risk capacity act as separate constraints and therefore, the risk profile or risk tolerance for an investor should reflect the lower of the investor’s willingness to accept risk and the investor’s ability to withstand declines in the value of their portfolio.

Some questionnaires only consider an investor’s willingness to accept risk without adequately considering risk capacity. While risk attitude is a key consideration, suitability is not just about making investment recommendations that reflect a customer’s attitude to risk.4 Therefore, a questionnaire should address both risk attitude and risk capacity. For illustrative purposes, a sample questionnaire that illustrates an approach to capturing both risk attitude and risk capacity is included in Appendix A.

There are several different aspects of risk attitude that can be assessed in a questionnaire.

Comfort with Risk – Some individuals possess psychological traits that allow them to accept taking greater risk.5 These individuals often view risk as an “opportunity” rather than focusing on the potential for loss. Questions that address an individual’s comfort with risk often involve choosing among different risk/return trade-off scenarios or simply asking the client to state their comfort level with risk.

Investment Choice – Preferences for different kinds of investments can also help to assess risk attitude, for example, the safety of a savings account versus the risk/ return potential of investing in the stock market. However, it is important that questions of this nature avoid using financial jargon to ensure that clients understand the questions asked.

Loss Aversion – Loss aversion questions gauge whether individuals focus on losses or gains or ask how much the value of the individuals’ investments could go down before they would begin to feel uncomfortable. Research indicates that loss aversion questions should be used in determining a client’s portfolio allocation preference and that proper assessment of loss aversion is essential to assessing whether clients are capable of maintaining asset allocations following a decline in equity markets.6

Regret and Anxiety – Individuals who are particularly prone to regret and anxiety tend to make decisions that are less likely to cause these emotions. In an investment context, these individuals may have greater comfort with conservative investment choices. Questions that measure regret and anxiety usually attempt to assess how a client would react after an investment declines.

Information that may be gathered in a questionnaire to help establish a client’s capacity to withstand risk includes financial information such as the amount of assets and debt that the client has accumulated, the client’s annual income and information regarding the stability of their income.

Determining how much of a client’s total investments a particular investment account represents is also an important consideration in assessing capacity for risk and ability to withstand loss. Other possible questions to measure risk capacity that are employed in some questionnaires include the number of dependents and whether or not the client has an emergency fund in place.

Age can also be an important consideration when assessing a client’s capacity to withstand loss. Younger clients who also have a long investment time horizon have more time to recover from losses and therefore may have the capacity to withstand more risk. Age may also impact the client’s willingness to accept risk as discussed above. While older clients can still have a wide distribution of risk tolerances from highly conservative to highly risk-tolerant, risk tolerance typically declines with age.

A study and analysis of personal financial risk tolerance found that individuals over age 60 had the lowest risk tolerance of the age-based sub-groups and also exhibited the smallest variation in scores.7 An AARP and ACLI survey found that retirees are highly loss averse.8

The questions included in an investor questionnaire should be evaluated for their understandability and their ability to differentiate between individuals with different levels of risk tolerance. Questions should be clear and avoid complex language and the use of financial jargon. Some have found that questions involving percentage rates of return can be problematic for certain investors.9

Research indicates that graphical presentation of questions increases the chance that an investor will understand the hypothetical choices and give a response more related to his or her true risk tolerance.10 Presenting the hypothetical gains and losses associated with different investment choices graphically or in dollar terms in addition to percentage terms may increase the likelihood that the investor will understand the choices.

Where questions use dollar figures, the amounts should be relevant and meaningful to the investor. Several questions in the sample questionnaire in Appendix A use $10,000 as the amount of a hypothetical investment. However, when dealing with clients with substantial assets an example of $10,000 may not be sufficiently meaningful and therefore the Approved Person should ask the client to complete the question using figures that are more relevant. For example, multiplying the $10,000 by 10 and assuming an investment of $100,000 and multiplying the dollar value of any gains and losses accordingly.

When determining the number of questions to include, it is generally accepted that an effective questionnaire should include multiple questions covering different elements of risk tolerance as discussed in Part III, A above. The fewer the questions included in a questionnaire, the greater the probability is of making an inaccurate assessment. However, it has also been noted that it is important to keep in mind that a questionnaire need not be too long.11 An overly lengthy questionnaire can result in respondents becoming fatigued and less engaged. Accordingly, a proper balance should be found so that the questionnaire provides for an adequate multi-dimensional assessment, yet can still be completed in a limited and reasonable amount of time.

A proper KYC and suitability process requires Members and Approved Persons to gather information on a client’s willingness and ability to accept risk, investment objectives, investment knowledge and time horizon and consider each of these pieces of information in determining suitable investment recommendations. Some poorly designed questionnaires aggregate information on different factors together in such a way that the value of each of the distinct pieces of information is lost or not adequately considered. With improper design, weighting or scoring this can result in clients being placed in a more aggressive risk profile than is indicated by the client’s specific answers to the questions directly pertaining to their risk tolerance. Members and Approved Persons should be able to demonstrate how a recommendation or transaction is suitable for a particular client given each of the constituent parts of the suitability assessment.

A sample questionnaire that illustrates an approach to collecting and considering each of the KYC elements in a questionnaire is included as Appendix A to this paper. The sample provided represents one possible approach that could be implemented by Members; however there are many different approaches that could achieve the same principles described in this paper.

Where a Member elects to implement the use of any questionnaire in their KYC process, including implementing the sample provided, they are encouraged to discuss their plans with MFDA staff prior to implementation.

In most cases the output from a questionnaire is to categorize clients into one of several investor profiles or risk categories. Care should be taken to ensure that the profiles are clearly defined and are adequately differentiated. Careful thought should go into determining how many categories will be used. Too few categories can result in large gaps between the risk profiles of different categories. For example, where there are large differences in the proportion that can be invested in equities for consecutive risk categories; this may create large jumps in the amount of risk taken.

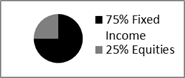

The descriptions of the categories should be presented in a way that explains the level of risk in a manner that is clear and not misleading. The description should clearly explain the expected composition of the investment portfolios for each investor profile or risk category. Pie charts are frequently used to help illustrate target asset allocations or model portfolios. The investor profile or risk category description should be reviewed with the client to help validate that an accurate assessment of their objectives and risk tolerance has been made.

The sample asset allocations in Appendix A are for illustration purposes and were developed based on a review of existing portfolio models in the industry. In addition to establishing asset allocations for the portfolios, it is also important that the risk of the portfolios is consistent with the investor profiles. Portfolio risk should be calculated using the standard industry risk methodology for mutual funds and should be monitored on a regular basis. In establishing asset allocations, Members should be able to demonstrate to regulators and others how they are suitable for each of the profiles.

Well-designed questionnaires effectively identify clients who are best suited to only placing their money in savings accounts, money market funds or GICs. A key element of an effective questionnaire is to identify those clients who are unwilling to take any risk with their capital and therefore should not consider anything other than the safest investment products. One way Members have addressed this is to incorporate procedures whereby if a client responds to any of the risk attitude questions indicating that they are not willing to accept any risk the tool stops there and defaults the client to a “very conservative” or “safety” profile.

Where a questionnaire is used, a critical step in the process is to validate the outputs and identify inconsistencies or contradictions in responses. A well-designed questionnaire will generally include several questions that test the investor’s willingness to accept risk and thus help to validate the client’s responses and reduce the risk of an inaccurate assessment. Contradictions in responses should be discussed with the client in detail to ensure questions have not been misinterpreted and to further reduce the risk of an inaccurate assessment. For example, if a client responds to a risk attitude question indicating that they are willing to take significant risk and then in a subsequent question the client responds in the most risk averse manner this contradiction should be discussed with the client.

There are also often situations where a client’s needs conflict with the level of risk that they are willing and able to take. In these circumstances, the Approved Peron should discuss this conflict in detail with the client. Clients may have unrealistic expectations, such as the expectation to earn high returns with little risk. A desire to meet unrealistic expectations may lead clients with a lower risk tolerance to invest in higher risk products, which can have significant negative consequences for both the client and Approved Person. A detailed discussion of the relationship between risk and return is critical to establishing realistic expectations.

Approved Persons should not override the risk a client is willing and able to take on the basis that the client’s needs or return expectations cannot be met by the selection or profile associated with their questionnaire responses. The Approved Person should identify any mismatches in the client’s objectives, risk tolerance and capacity for loss. The questions that generated the conflict should then be revisited with the client. Where a client’s goals or return objectives cannot be achieved without taking greater risk than they are able or willing to take, alternatives should be clearly explained such as saving more, spending less or retiring later. Where after discussion, it is determined that the client does not have the capacity or tolerance to sustain the potential losses and volatility associated with a higher risk portfolio, the Approved Person should explain to the client that their need or expectation for a higher return cannot realistically be met.

A separate KYC form that collects risk tolerance, investment knowledge, investment objectives and time horizon should not be necessary where this information is adequately captured within the questionnaire itself. However, other information that is not typically collected in a questionnaire must still be collected if required under MFDA requirements and other applicable regulations. This information is typically collected on a new account application form (“NAAF”) and includes:

In addition to the information specifically collected on the NAAF and questionnaire, there may be other relevant matters discussed during the KYC process. A questionnaire should be part of a broader discussion with the client about the client’s circumstances and overall investment goals. This may include a discussion about specific client circumstances (for example, divorce, serious illness, job loss) and the client’s investment goals (for example, funding a child’s education or purchasing a house). In the case of senior investors in particular, some issues to consider may include the client’s sources of income, housing plans and any significant health care costs.

The literature recommends that a questionnaire be repeated with the client every two to three years to properly understand their current financial risk tolerance.12 In addition, the questionnaire should be completed again when there are major changes in the client’s financial circumstances and after any significant life events such as the death of a partner or divorce. Advisors may also wish to repeat the questionnaire when significant changes in market conditions occur or clients express concern about the value of their investment account. The process of repeating the questionnaire every few years and when significant events occur can be useful not only to determine if the client’s attitude toward risk or capacity to withstand losses has changed, but also to help client’s stay focused on their financial goals and adhere to their long-term investment plans despite market volatility.

A key consideration when implementing a questionnaire is determining how the questionnaire will work with the Member’s back-office system. In most cases, where Members have implemented questionnaires, the implementation necessitated changes to their existing back office system.

The back-office system should be capable of capturing the responses and information collected on the questionnaire as these responses establish the client’s KYC information including their risk tolerance, investment objectives and time horizon.

A questionnaire is most effective when it is fully integrated into the back office system. Full integration with the back-office system can include automated controls, scoring, validations and the highlighting of inconsistencies in responses. For example, some Members have implemented effective procedures by automating their questionnaires to:

Testing of the system functionality and controls should also take place prior to implementation to ensure data is accurately captured, scores are accurately calculated and to validate any automated logic checks or controls.

Certain investment strategies, including borrowing to invest and investing in exempt securities require additional supervision and scrutiny. Additional information that is not commonly included in most questionnaires (including the sample provided in this paper) must be collected and assessed when recommending these strategies. This includes specific details and figures for the client’s financial assets, net worth, annual income and monthly debt and lease obligations.

In addition, the Member should develop procedures that specifically address how the responses to specific questions will be used in the suitability assessment. Some questions, such as the question on time horizon, may directly translate to the Member’s existing leverage supervision criteria while others will pose additional challenges and require further internal guidelines and procedures.

For example, if using the sample questionnaire provided, the Member may decide that only those investors with a risk attitude score over 25 are suitable candidates for leverage. In addition, the Member may further decide that clients who select the most risk averse answer to any of the questions in the risk attitude section would not be suitable candidates for leverage.

Typically an investor questionnaire is used in conjunction with an approach that categorizes clients into various investor profiles and then matches them to pre-established model portfolios. Members using this approach have to be able to demonstrate using statistical analysis that the pre-established portfolios are suitable for the clients within each category. Members often engage a registered portfolio manager to construct and monitor the model portfolios.

We have observed several different approaches to constructing pre-established model portfolios for investor profiles. These include single fund solutions, set portfolios of particular funds or the ability to select from a list of specific funds representing various categories or asset classes.

An approach that allows advisors to select any fund from a broad asset category is the most challenging from a supervisory perspective and typically requires the Member to test various “worst-case” scenarios using the most volatile funds in particular groups or asset classes. In addition, the asset allocation limits typically need to be more conservative under this structure to ensure the various combinations of funds still result in a suitable portfolio for a given risk tolerance or investor profile.

Ongoing testing of model portfolios should be performed to ensure the volatility of the model portfolios remains reasonable for the specific risk categories.

Where a questionnaire results in model portfolios or asset allocation targets, it is reasonable to have procedures to rebalance clients on a regular basis to the target allocation. However, Members should consider how any rebalancing will be conducted; bearing in mind that discretionary trading is not permitted under MFDA Rules. Accordingly, the Member’s procedures should not lead to any unauthorized trading. MFDA Rules require that client instructions be obtained for all transactions.

Supervisors play a vital role in ensuring that questionnaires are properly completed and that clients are suitability invested. As with the completion of any KYC documentation, supervisors should ensure that forms are completed in their entirety and signed and dated by the client. Supervisors should also review the questionnaire for any contradictions or inconsistencies in responses as discussed in Part IV, A; and should ensure clear documentation is maintained demonstrating how any inconsistencies were resolved.

The type of questionnaire and scoring system implemented will also determine the specific supervisory procedures required. For example, if a point scoring system has been implemented, there should be a supervisory check to ensure the score is accurately calculated. Where a table or matrix approach to determining investor risk profiles has been implemented (such as the sample questionnaire provided in Appendix A), there should be supervisory controls in place to ensure responses have been appropriately carried forward and allocated under the correct risk profile category. This step is of critical importance. Electronic questionnaires with automated calculations and controls can reduce the burden on supervisors and significantly mitigate or eliminate the risk of incorrect calculations and ensure that responses are carried forward correctly.

The successful implementation of any new approach is dependent on the quality of training provided to Approved Persons and supervisory staff. Prior to implementing an investor questionnaire, detailed training should be conducted that explains the methodology and the expectations for Approved Persons and supervisors when using the questionnaire.

Inadequate training can result in a variety of concerns including:

Approved Person training should concentrate on the process for completing the questionnaire with clients and focus on the purpose of the questions, how to engage clients and guide them through the process and the discussions that should be had with clients where inconsistencies are identified. The Approved Person should also fully understand how the client responses lead to the risk profile and investment portfolio recommended. Training for supervisors will differ depending on the type of questionnaire implemented and whether or not the process is manual or electronic but should include procedures to review for reasonableness and consistency.

There are a number of different approaches to collecting know-your-client information and assessing risk tolerance that can be effective and meet the regulatory requirements. An investor questionnaire is just one example of a reasonable approach to satisfying the KYC obligation. However, when properly implemented, a questionnaire approach can have significant benefits for investors, Members and Approved Persons including helping to ensure suitable investment recommendations.

A questionnaire helps to provide structure and consistency in the approach to collecting KYC information and assessing risk tolerance. The use of a structured questionnaire format rather than an unstructured or semi-structured interview format can increase the likelihood of making an accurate assessment of risk tolerance.13

In addition, an investor questionnaire can help to illustrate the relationship between risk and return and make the process for determining suitable investment recommendations more transparent and easily understood for clients. Greater client understanding of the relative risks of investments products and the trade-off between risk and return can help provide a common understanding and lead to realistic client return expectations.

An accurate assessment of client risk tolerance is not only critical to meet regulatory obligations but can also have additional benefits. Investor returns are often decreased because of the tendency to pull money out of investments after a market decline and conversely invest more after a market increase. However, financial advice can play a significant role in improving long-term investment performance and helping investors avoid ill-timed movements in and out of markets. Canadian and international studies have demonstrated the value of financial advice. These studies have shown that clients, who use a financial advisor save more, accumulate more wealth and better adhere to long-term investment decisions despite market volatility than those who do not use a financial advisor.14,15 A proper assessment of risk tolerance is essential to developing suitable investment recommendations and an asset allocation that investors will be more likely to adhere to through market fluctuations thus avoiding ill-timed movements in and out of markets.

While there are many benefits to the use of investor questionnaires there are also limitations. Firstly, the results of questionnaires should not be used as a replacement for the discussion between the Approved Person and the client. Rather, a questionnaire should help to support that discussion and allow for a deeper examination of the client’s goals, investment preferences and the relationship between risk and return.

In addition, even a good questionnaire can occasionally produce inaccurate results. The results of the questionnaire should always be discussed with the client to obtain their confirmation (or otherwise) of the resulting investor profile. Such discussion can, as a by-product, lead to a more in-depth understanding of the client.

Lastly, while the sample provided in Appendix A provides an example of a questionnaire and sample investor profile descriptions, any questionnaire and resulting investor profiles should be customized by the Member to reflect the investment choices offered by the Member.

As noted in the introduction, the purpose of this paper is to promote further discussion on a topic of interest to many Members. MFDA staff has worked closely with Member firms who have implemented investor questionnaires and provided guidance throughout the implementation process. Accordingly, if a Member is considering implementing a questionnaire or otherwise making significant changes to their approach to collecting KYC information or assessing suitability, the Member should discuss the proposal with MFDA staff prior to implementation to obtain specific guidance.

The sample questionnaire and investor profiles provided are for illustrative purposes only. A questionnaire or similar instrument is only part of the full know-your-client process. Any questionnaire and accompanying investor profiles should be customized to the dealer’s investment platform and product offerings. None of the information in the sample questions or investor profiles is intended as general or specific investment advice and should not be used for that purpose. In establishing asset allocations, Members should be able to demonstrate to regulators and others how they are suitable for each of the profiles.

Investment Time Horizon: The length of your investment time horizon impacts the types of investments that may be suitable for you. Investors with a time horizon of greater than three years have a greater degree of flexibility when building a portfolio (although risk tolerance and investment objectives must also be considered). If you have a very short time horizon, more conservative investments like GICs or money market funds may be the only suitable option for you.

1. When do you expect to need to withdraw a significant portion (1/3 or more) of the money in your investment portfolio?

Investment Knowledge: If you have a high level of investment knowledge, you have a good understanding of the relative risk of various types of investments and understand how the level of risk taken affects potential returns. If you have very little knowledge of investments and financial markets, speculative and high risk investments and strategies are likely not suitable options for you.

2. Which statement best describes your knowledge of investments?

Investment Objectives: Investment objectives are the goal or result you want to achieve from investing. Understanding your investment goals helps determine the types of investments best suited to meet your needs. The investment products used to meet different goals have varying levels of risk and potential returns.

3. What is your primary goal for this portfolio:

Risk Capacity (Questions 4-9): Your financial situation including your assets, debt and the amount and stability of your income are all important when determining how much risk you can take with your investments. In addition, the larger the portion of your total assets that you are investing, the more conservative you might wish to be with this portion of your portfolio.

4. What is your annual income (from all sources)?

5. Your current and future income sources are:

6. How would you classify your overall financial situation?

7. What is your estimated net worth (investments, cash, home and other real estate less mortgage loans and all other debts)?

8. This investment account represents approximately what percentage of your total savings and investments. (Total savings and investments include all the money you have in cash savings, GICs, savings bonds, mutual funds, stocks and bonds)?

9. What is your age group? (Your age is an important consideration when constructing an investment portfolio. Younger investors may have portfolios that are primarily invested in equities to maximize potential growth if they also have a higher risk tolerance and long investment time horizon. Investors who are retired or near retirement are often less able to withstand losses and may have portfolios that are invested to maximize income and capital preservation)

Your score for questions 4-9

Risk Attitude (Questions 10-15): Your comfort level with risk is important in determining how conservatively or aggressively you should invest. Generally speaking, you need to consider accepting more risk if you want to pursue higher returns. If you decide to seek those potentially higher returns, you face the possibility of greater losses.

10. In making financial and investment decisions you are:

11. The value of an investment portfolio will generally go up and down over time. Assuming that you have invested $10,000, how much of a decline in your investment portfolio could you tolerate in a 12 month period?

12. When you are faced with a major financial decision, are you more concerned about the possible losses or the possible gains?

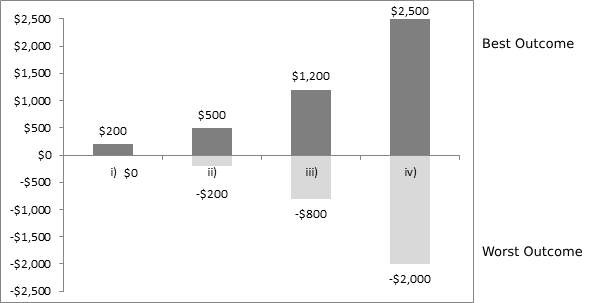

13. The chart below shows the greatest one year loss and the highest one year gain on four different investments of $10,000. Given the potential gain or loss in any one year, which investment would you likely invest your money in:

Range of Possible Outcomes in 1 Year

14. From September 2008 through November 2008, North American stock markets lost over 30%. If you currently owned an investment that lost over 30% in 3 months you would:

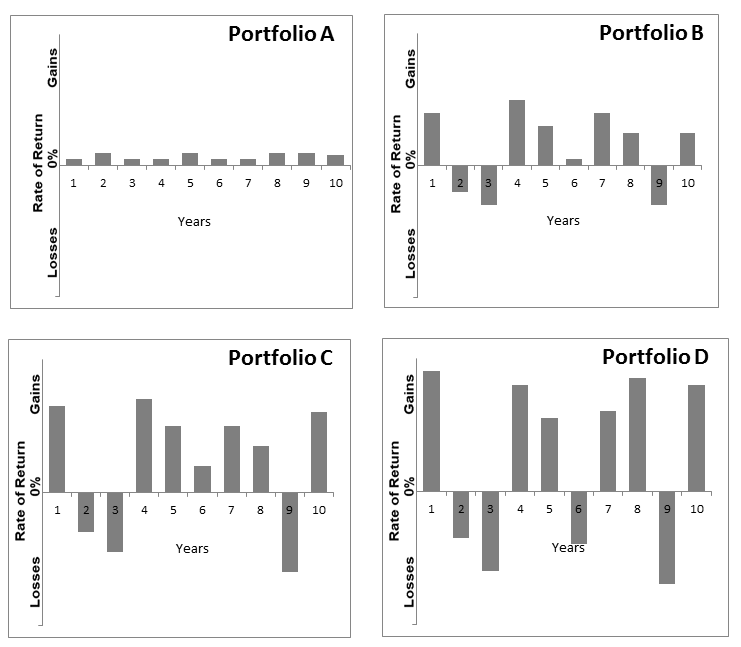

15. Investments with higher returns typically involve greater risk. The charts below show hypothetical annual returns (annual gains and losses) for four different investment portfolios over a 10 year period. Keeping in mind how the returns fluctuate, which investment portfolio would you be most comfortable holding?

Your score for questions 10-15

On the table below circle your answers to the time horizon, investment knowledge and investment objectives questions and your total scores for the risk capacity and risk attitude questions.

Your investor profile is determined by the circle that is in the column furthest to the left in the table.

Questions | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|

| Time Horizon (question 1) | i | ii |

| iii, iv | v |

| Investment Knowledge (question 2) |

|

| i | ii | iii |

| Investment Objectives (question 3) | i | ii | iii |

| iv |

| Risk Capacity (total of questions 4-9) |

| <15 | 15-25 | 26-40 | >40 |

| Risk Tolerance (total of questions 10-15) | <20 | 20-24 | 25-30 | 31-45 | >45 |

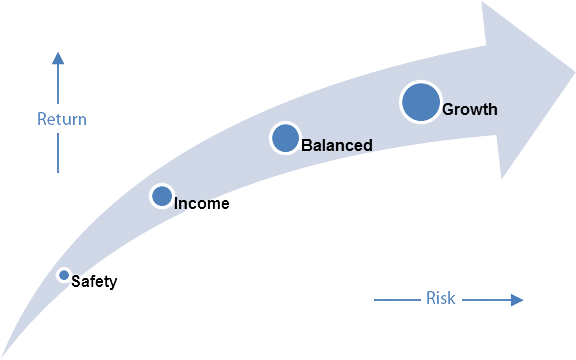

| 1. Very Conservative You have a very low tolerance for risk and are unable to tolerate any investment losses or you have a very short investment time horizon. You prefer knowing that your capital is safe and are willing to accept lower returns to protect your capital. | Asset Allocation

|

| 2. Conservative Income You have a low tolerance for risk and potential loss of capital or a short investment time horizon. You are willing to accept some short term fluctuations and small losses in your investment portfolio in exchange for modest returns. The primary objective of your investment portfolio will be to provide income by investing primarily in funds that invest in fixed-income securities. While capital appreciation is not a priority, a small portion of the portfolio may be invested in equity funds to provide the potential for some growth to offset the impact of inflation. | Asset Allocation

|

| 3. Balanced You have a moderate tolerance for risk and loss of capital. You are willing to tolerate some fluctuations in your investment returns and moderate losses of capital. You have at least a medium term investment time horizon. The objective of your portfolio will be to provide a combination of income and long term capital growth and therefore the portfolio will include at least 40% in fixed income investments. | Asset Allocation

|

| 4. Growth You have a high tolerance for risk and loss of capital. You are willing to tolerate large fluctuations in your investment returns and moderate to large losses of capital in exchange for potential long-term capital appreciation. You do not have any significant income requirements from your investments. You have at least a medium term investment time horizon. | Asset Allocation

|

| 5. Aggressive Growth Your tolerance for risk, portfolio volatility and investment losses is very high. You are willing to tolerate potentially significant and sustained price fluctuations and large losses of capital. You have extensive investment knowledge. You have no income requirements from your investments and have a long investment time horizon. | Asset Allocation

|

On the table below circle your answers to the time horizon, investment knowledge and investment objectives questions and your total scores for the risk capacity and risk attitude questions.

Your investor profile is determined by the circle that is in the column furthest to the left in the table.

Questions | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|

| Time Horizon (question 1) | i | ii | iii, iv | v | |

| Investment Knowledge (question 2) | i | ii | iii | ||

| Investment Objectives (question 3) | i | ii | iii | iv | |

| Risk Capacity (total of questions 4-9) | <15 | 15-25 | 26-40 | >40 | |

| Risk Tolerance (total of questions 10-15) | <20 | 20-24 | 25-30 | 31-45 | >45 |

In this example, although the client expressed a willingness to accept risk, they have very limited risk capacity (ability to withstand losses). The client’s Risk Capacity is the most constraining element, leading to a Conservative Income profile.

Questions | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|

| Time Horizon (question 1) | i | ii |

| iii, iv | v |

| Investment Knowledge (question 2) |

|

| i | ii | iii |

| Investment Objectives (question 3) | i | ii | iii |

| iv |

| Risk Capacity (total of questions 4-9) |

| <15 | 15-25 | 26-40 | >40 |

| Risk Tolerance (total of questions 10-15) | >20 | 20-24 | 25-30 | 31-45 | <45 |

In this example, the client has significant financial resources but is unwilling to take any risk with their investments. The client’s Risk Attitude is the most constraining element, leading to a Safety profile.

Welcome to CIRO.ca!

You can find the Canadian Investment Regulatory Organization (CIRO) at CIRO.ca with our fresh look and feel.