Alert:

For more information on the cybersecurity incident, please visit the cybersecurity incident page.

Since the publication of this Bulletin, the MFDA has made amendments to its Rulebook implementing the Trusted Contact Person (TCP) requirement and Temporary Hold regulatory framework. These amendments came into effect December 31, 2021. Please review Bulletin #0895-P for further information.

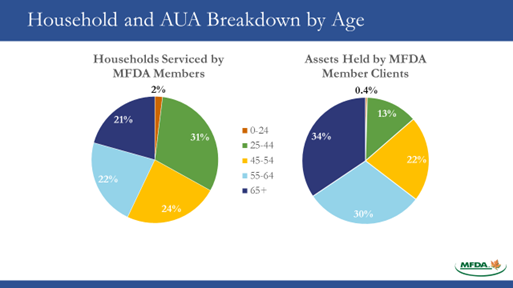

Seniors are a rapidly growing demographic in Canada. Average life expectancy of Canadians is rising and by 2036, seniors have been projected to account for between 23% to 25% of the Canadian population1. Research conducted by the MFDA indicates that clients 65 years of age or older account for 21% of all households serviced by MFDA Members and 34% of Member Assets Under Administration (“AUA”). The MFDA is committed to addressing issues impacting senior investors and assisting Members and Approved Persons in servicing this important segment of Canadian investors.

MFDA Members have been seeking enhanced guidance and education on serving aging investors and vulnerable clients, as expressed through the MFDA Member Outreach Initiative (see MFDA Bulletin #0792 – M). In response, MFDA staff is developing additional tools and guidance on servicing and protecting senior investors, including holding a third Seniors Summit on October 30, 2019.

This bulletin provides guidance on practices that can be implemented to assist in the protection of seniors and vulnerable clients. In addition, attached at Appendix “A” are the key learnings from the 2015 Seniors Summit which will be updated with further information from the 2019 Seniors Summit. We encourage Members to review these materials.

MFDA staff have observed practices at certain Members related to the protection of seniors and vulnerable clients, specifically: (1) requesting clients to name a trusted contact person (TCP); and (2) placing a temporary hold on transactions where there are reasonable concerns regarding financial exploitation of a client or a client’s mental capacity. Set out below are recommendations in respect of TCP and placing temporary holds on transactions, based on these practices.

Members may consider taking reasonable steps to obtain the name and contact information of a TCP from their clients. A Member that decides to implement a TCP process should consider asking Approved Persons to request their clients to name a TCP at the time of account opening, and to confirm or update the TCP information periodically; for example, during a KYC update.

Members and Approved Persons should be aware that the TCP is a complement to, and not a substitute for, a Power of Attorney (POA). The TCP does not have decision making power with respect to, or authority to effect changes to, the client’s account by virtue of being the TCP.

Contacting a TCP could be of assistance to Members in situations where, among others, there are concerns that a client is being financially exploited or concerns regarding the client’s mental capacity.

When obtaining a TCP, Members should provide the client with written notice of the circumstances in which a TCP may be contacted and obtain the client’s written consent to disclose any personal information that may be shared with the TCP in those situations, as required by MFDA Rule 2.1.3 (Confidential Information) and privacy legislation.

The TCP should be an individual over the age of majority. As a matter of good practice, the TCP should generally not be an individual who has an interest in the client’s account and should not be involved in making financial decisions with respect to the account, such as a POA. Members and Approved Persons should encourage their clients to name different individuals as their TCP and POA, however, it is recognized that this may not be possible for all clients.

When a decision is made to contact a TCP, Members should consider whether other relevant parties such as the MFDA, the police or an office of a public guardian or trustee in the relevant jurisdiction should be contacted.

The following outlines guidance on the general MFDA approach to placing temporary holds on transactions in the circumstances set out below.

Members may develop policies and procedures to enable the dealer to place a temporary hold on a transaction where there is a reasonable concern that financial exploitation of the senior or vulnerable client is taking place, or will take place, or a reasonable concern regarding the mental capacity of the client related to financial decision making. The obligation to deal fairly, honestly and in good faith with clients pursuant to MFDA Rule 2.1.1 (Standard of Conduct) applies when placing temporary holds.

The decision by a Member to place a temporary hold should only be made by authorized and qualified supervisory and compliance staff. Approved Persons who believe that a temporary hold should be placed on a transaction should follow their Member’s policies and procedures regarding the placement of temporary holds by the Member.

Members that place temporary holds should have policies and procedures in place to address matters that include identifying supervisory and compliance staff authorized to: (1) place a temporary hold on behalf of the Member; (2) review, monitor or address the issues in relation to the hold; and (3) decide to complete or disallow the transaction subject to the temporary hold.

When the Member makes the decision to place a temporary hold, the Member or Approved Person should notify the client, and where appropriate, contact the TCP and any parties authorized to transact on the account, such as a POA, as quickly as possible. The temporary hold should not last longer than necessary to address the concern and the Member or Approved Person should update the client as necessary.

In an effort to resolve the matter as quickly as possible, the review of the concern that prompted the hold should begin on a timely basis. Once the review has been completed, the Member should make the decision to complete or disallow the relevant transaction and notify the client.

Members and Approved Persons are reminded that they should maintain appropriate documentation and records in sufficient detail to evidence the following: (1) the reasonable concerns that prompted the temporary hold; (2) the review conducted; and (3) its conclusion.

Further discussion of TCP and temporary holds will take place at the 2019 Seniors Summit on October 30, 2019. MFDA staff advises that it is also currently developing additional guidance and resources in this area.

In addition, the MFDA is actively engaged with the CSA in developing a flexible and responsive regulatory approach to address issues of financial exploitation and diminished mental capacity among seniors and vulnerable clients.

Appendix "A"

Key Learnings

Delivered by:

Watch: Medico-Legal Issues in Servicing Senior Clients

Summary: Dr. Carole Cohen and Arthur Fish discuss the medical and legal implications of capacity when dealing with senior clients. Dr. Cohen provides red-flags and indicators that may identify a mental capacity issue, and Arthur Fish discusses how to deal with capacity issues from a legal context.

Diminished Capacity

Diminished Capacity is a complex medical/legal construct. It is situation specific, meaning it is not an all or nothing concept and it is often related to the specific task or issue in question. For example, an individual may lack the capacity to make financial decisions but may still maintain capacity to make health decisions. Even a diagnosis of dementia does not in itself mean that a person lacks capacity to make decisions. The focus always has to be on the specific context and the facts.

Approved Persons cannot make a determination as to whether an individual lacks mental capacity, however, there are red-flags to be aware of that may indicate mental capacity issues.

Diminished Capacity – Red Flags

Consider the four “C”s

Red Flag Examples

Elder Financial Abuse

There is an increased risk of financial abuse and exploitation among older clients. The abuse is more likely to be carried out by family members or caregivers than strangers.

Risk Factors for Financial Abuse

Observable Red Flags

Questions you can ask the client

When a POA is in place, it is important to remember that the appointed attorney has fiduciary responsibilities towards the client and that there could be legal exposure to knowingly participating in a breach of that fiduciary duty. For example, processing a large redemption requested by a POA that is clearly not for the benefit of the client.

First question you should ask when POA is presented is “why?”. It is also important to clarify who reporting should go to once a POA is in place and to set timelines for how long the POA will be in place. These may differ depending on the reason for the POA. (e.g. client away on vacation vs. client is losing capacity). If a POA is being put in place because of loss of capacity this would be a time to update KYC information.

Panel Discussion

Moderator:

Panelists:

Watch: Advising During Depletion Phase

Summary: Panel members discuss challenges associated with advising retirees and explore strategies for advising during the decumulation phase.

Delivered by: Ron Long, Director of Regulatory and Elder Client Initiatives – Wells Fargo Advisors, LLC

Watch: Facing Elder Financial Abuse

Summary: Mr. Long provides an overview of his firm’s compliance practices related to detecting and preventing elder financial abuse.

| What to do | Additional Detail |

|---|---|

| Observe |

|

| Wonder why |

|

| Negotiate |

|

| Isolate |

|

| Tattle |

|

Delivered by: Goshka Folda, President and CEO – Investor Economics

Watch: The Aging Canadian Demographic

Summary: Ms. Folda presents how Canadian demographics are shifting, the impact that these shifts are going to have on dealer business and the new risks and realities of senior clients and their finances.

Delivered by: Dan Sibears, Executive Vice-President, Regulatory Operations/Shared Services – FINRA

Watch: FINRA and Seniors’ Issues

Summary: Mr. Sibears discusses best practices for seniors seen at FINRA member firms as well as FINRA’s seniors initiatives including their Securities Helpline for Seniors, and their proposed rules on trusted contact person and a safe harbour for temporary holds on disbursements.

Best practices regarding seniors issues seen at FINRA regulated firms:

Future FINRA Policy Initiatives (in place as of 2018):

Welcome to CIRO.ca!

You can find the Canadian Investment Regulatory Organization (CIRO) at CIRO.ca with our fresh look and feel.