Alert:

For more information on the cybersecurity incident, please visit the cybersecurity incident page.

IIROC is proposing amendments to the IIROC Rules and to Form 1 (collectively, the Proposed Amendments) regarding the floating index margin rate methodology (the Methodology) applicable to qualifying Canadian and U.S. index products. The primary objective of the Proposed Amendments is to reduce procyclicality in IIROC’s Methodology.

Procyclical requirements or practices are those that are positively correlated with business or credit cycle fluctuations and that may cause or exacerbate financial instability. Margin rules that stipulate lower margin requirements during periods of low volatility and higher margin requirements during periods of high volatility are procyclical.

The Proposed Amendments:

Impacts

We anticipate the Proposed Amendments will generally benefit Dealers, clients, and other stakeholders.

The benefits of reducing procyclicality are generally recognized and can be summarized as promoting financial stability and resiliency in periods of high market volatility. We believe these benefits outweigh the opportunity costs associated with reduced leverage during periods of low market volatility.

How to Submit Comments

Comments on the Proposed Amendments should be in writing and delivered by June 27, 2022 (60 days from the publication date of this notice) to:

Member Regulation Policy

Investment Industry Regulatory Organization of Canada

Suite 2000

121 King Street West

Toronto, Ontario M5H 3T9

e-mail: memberpolicymailbox@iiroc.ca

Also, provide a copy to the Recognizing Regulators by forwarding a copy to:

Market Regulation

Ontario Securities Commission

Suite 1903, Box 55

20 Queen Street West

Toronto, Ontario M5H 3S8

e-mail: marketregulation@osc.gov.on.ca

Commentators should be aware that a copy of their comment letter will be made publicly available on the IIROC website at www.iiroc.ca.

IIROC Rules set out minimum margin rates for various investment products. In most cases, these margin rates are fixed percentages. In the case of qualifying Canadian and U.S. index products, these rates are determined using a prescribed formula, which is the foundation for IIROC’s Methodology.

Subsection 5130(9) of the IIROC Rules includes definitions for the terms “floating margin rate” and “regulatory margin interval”. The floating margin rate for a qualifying index product is determined according to the regulatory margin interval, which is a prescribed formula detailed in section 5360. The formula:

IIROC publishes a monthly list of floating and tracking error margin rates for qualifying Canadian and U.S. index products (floating margin rate list), whose index qualifies under the definition of an “index” in subsection 5130(9). We maintain a dedicated web-page for this list, where users can find the list and review relevant information related to the Methodology.

There are currently 12 qualifying Canadian indices (3 broad based and 9 sector) and 11 qualifying U.S. indices (all broad based) on the list. IIROC calculates the regulatory margin interval for eligible index participation units (IPUs) and qualifying baskets of index securities that passively track these indices and hold the underlying securities. Eligible IPUs and exchange traded funds (ETFs) must achieve correlation to their qualifying index by investing in the underlying securities in substantially the same proportion as those securities are reflected in the index. Appendix E includes currently eligible IPU/ETF symbols for each qualifying index.

We also calculate regulatory margin intervals for the tracking error resulting from recognized offset strategies for:

Section 5360 details the specific requirements for a qualifying basket of index securities. The floating margin rate list web-page includes a section that details characteristics of ineligible IPUs and ETFs that may be based on a qualifying index. Rule 5700 details recognized offset position requirements.1

The IIROC rules do not include discretionary margin-setting authority for securities. The Proposed Amendments introduce floor margin rates for individual and offset positions and codify IIROC’s discretionary authority to modify the regulatory margin interval calculation in limited circumstances to ensure appropriate margin requirements. We believe these Proposed Amendments are necessary to properly maintain the Methodology through various market cycles and volatility scenarios.

This approach aligns with IIROC’s margin-setting framework for futures contracts under section 5790, which follows a “greatest of” calculation methodology, and provides IIROC discretionary authority to set higher or lower margin rates as needed.

IIROC’s Methodology calculates lower than optimal margin rate requirements during long periods of low market volatility, but results in sharp increases in margin rates during intermittent periods of high market volatility. The Proposed Amendments are required to reduce this procyclicality in IIROC’s Methodology.

The blackline text of the Proposed Amendments to the IIROC Rules is set out in Appendix A and a clean copy of the changes is set out in Appendix C. The blackline text of the Proposed Amendments to Form 1 is set out in Appendix B and a clean copy of the changes is set out in Appendix D. We included a list of Canadian and U.S. qualifying indices in Appendix E.

Table 1 provides an overview of the proposed floor margin rates for qualifying Canadian and U.S. index products. These proposed rates will be set by IIROC at levels that are similar to the U.S. SEC Net Capital haircut rates for comparable index products as shown in section 2.2 below. We also analyzed historical regulatory margin interval data to support the proposed minimum floor margin rates, including the data presented in Figures 1 and 2 in section 2.1 below.

Table 1 – Proposed floor margin rates for qualifying Canadian and U.S. index products

| Proposed minimum requirements | Basket of index securities | Index participation units (IPU) and U.S. exchange-traded fund (ETF) equivalents | Tracking error offsets |

|---|---|---|---|

| IIROC minimum margin rate requirements for qualifying indices | Broad based index: 10% | Broad based index: 10% | Broad based index: 2% |

| Sector index: 15% | Sector index: 15% | Sector index: 3% |

We propose to amend subsection 5360(1), which sets out the minimum margin requirements for qualifying index products, to a “greater of” the floor margin rate and the floating margin rate percentage methodology. Qualifying baskets of index securities will still require additional margin, referred to as the incremental basket margin rate, where applicable.

We codified in new subsection 5360(3) that IIROC calculates a regulatory margin interval for index products on qualifying indices and we included the qualification criteria for a qualifying index. As with current practice, a qualifying index must:

We categorized qualifying indices as either a broad based index or a sector index, which required corresponding changes to the current index definitions in subsection 5130(9) and Form 1. The current definition for an index in subsection 5130(9) describes minimum requirements that are appropriate for a sector index, and Form 1 includes a definition for a broad based index. We updated the Form 1 definition and replicated it in subsection 5130(9) for ease of reference.

As a result, the proposed definitions for both index types appear in subsection 5130(9), with updates to each index type that:

Also, to ensure consistency in applying the broad based index definition, we amended subsection 5130(4) regarding the definition of foreign listed equity securities eligible for margin. We replaced “major broadly based index” with “major widely quoted market index” because we have not generally applied the prescriptive broad based index requirements to determine margin eligibility for foreign listed equity securities.

Proposed clause 5360(4)(ii) codifies IIROC’s discretionary authority to modify the regulatory margin interval calculation in limited circumstances.

We do not anticipate exercising this discretion in normal circumstances, including most instances where a calculated regulatory margin interval exceeds a floor margin rate. As noted in section 1.2 above, we believe limited discretion is necessary to properly maintain the Methodology through various market cycles, which include high market volatility scenarios.

The Proposed Amendments codify the discretion IIROC exercised in response to the extraordinary COVID 19 related market volatility in 2020. At that time, we adjusted the Methodology to mitigate margin rate procyclicality. We notified stakeholders when we adjusted the margin rate-setting process, and again when we normalized the process. Proposed clause 5360(4)(ii) requires IIROC to notify Dealer Members if any adjustments to the regulatory margin interval calculation are made.3

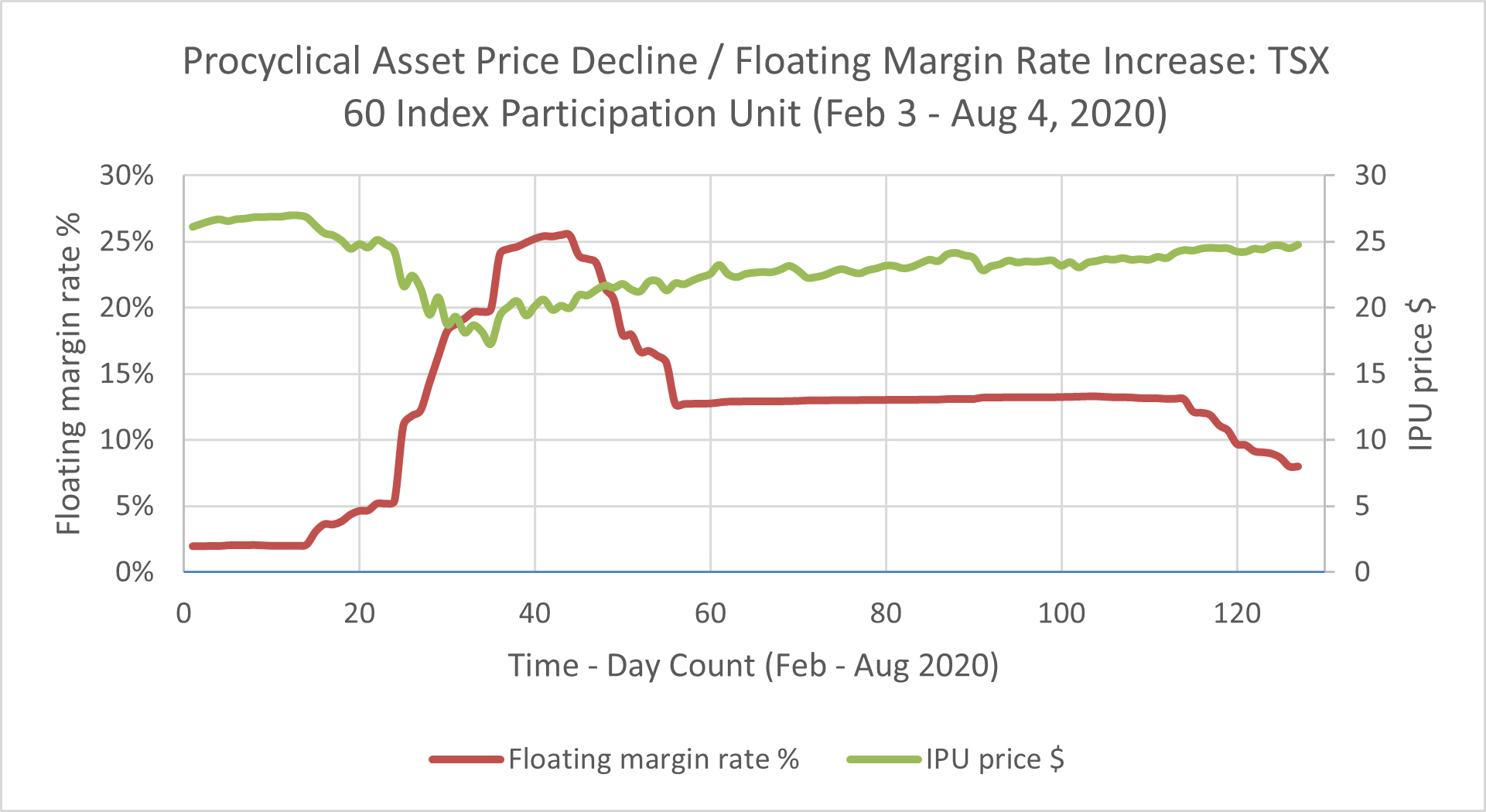

Sharp increases in floating index margin rates typically occur when the underlying asset prices are declining, which is a feature that may amplify the deleveraging impacts of margin rate procyclicality.

In February 2020, the TSX 60 IPU (XIU) floating margin rate dropped to a procyclical low of 2%. Figure 1 shows the subsequent market value decline in XIU, and corresponding increase in its floating margin rate, during the COVID 19 outbreak.

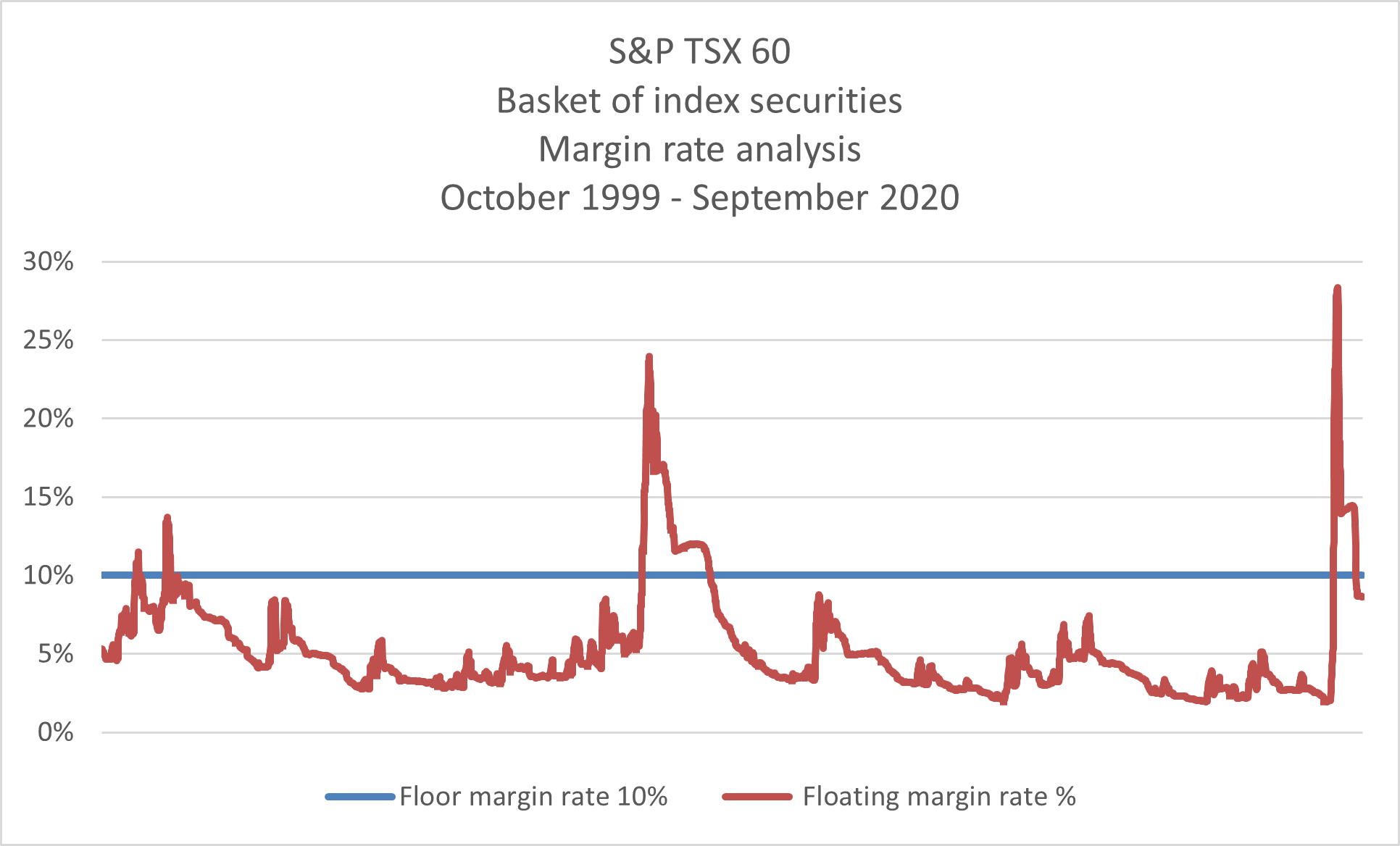

Figure 2 provides a longer term view of the TSX 60 basket of securities since 1999, demonstrating intermittent procyclical margin rate volatility. This procyclical margin rate volatility pattern occurs across all qualifying indices.

Figure 1 – TSX 60 Index participation unit (XIU) unit price and floating index margin during COVID outbreak

Figure 2 - S&P TSX 60 Basket of index securities – margin rate analysis 1999 - 2020

Table 2 provides a high-level overview of U.S. index product minimum margin requirements. The proposed minimum floor margin rates will be set by IIROC at levels that closely align with the U.S. SEC Net Capital haircut rates for comparable index products. Notably, the IIROC proposed tracking error floor margin rates are lower than the U.S. offset margin requirements because we are only proposing floor rates and will continue to calculate a regulatory margin interval.

Table 2– U.S. Index product minimum margin requirements

| Basket of index securities | Exchange traded funds (ETFs) | ETF and qualified baskets offset | |

|---|---|---|---|

| SEC Net Capital Haircut Rules | High-capitalization diversified indexes: (+)(-) 10%4 Narrow-based indexes, and non-high-capitalization diversified indexes: (+)(-) 15%5 | High-capitalization broad-based indexes: 10% Non-high-capitalization broad-based and narrow-based or sector indexes: 15% | Index ETF and qualified stock baskets for high-capitalization broad-based and narrow-based or sector indexes including the U.S. NASD Market index: 5% Index ETF and qualified stock baskets for non-high-capitalization broad-based indexes: 7.5% |

| FINRA Rules | Refers to SEC rules for Baskets | Initial margin: 50% Maintenance margin: 25% | Refers to SEC rules for Baskets |

In developing these proposals, we considered the following three alternatives:

We selected the Proposed Amendments because we believe it is a more straightforward approach that best addresses procyclical concerns. As part of our analysis for Alternative #2, we analyzed several potential modifications to the current regulatory margin interval calculation and determined that each of these potential modifications introduces complexity without necessarily resulting in a more effective volatility estimator. We also considered setting fixed margin rates (Alternative #3) but determined that it would be challenging to set appropriate fixed margin rates for the full range of market cycles, qualifying index products, and scenarios.

The Proposed Amendments do not impose any burden or constraint on competition or innovation that is not necessary or appropriate in furtherance of IIROC’s regulatory objectives and do not impose costs or restrictions on the activities of market participants (including Dealer Members and non-Dealer Members) that are disproportionate to the goals of the regulatory objectives sought to be realized.

The benefits of reducing procyclicality are generally recognized and can be summarized as promoting financial stability and resiliency in periods of high market volatility. We believe these benefits outweigh the costs associated with the Proposed Amendments. Dealer Members and clients will need to apply higher margin rates for qualifying index products during periods of low market volatility, but this impact is offset by the “initial buffer” protection this provides during periods of high market volatility.

We believe any potential impacts should be mitigated because common Dealer Member practices include:

We believe all stakeholders, including IIROC, will benefit from the greater stability that will result from the use of floor margin rates. We expect the operational burden of updating systems for margin rate changes will be significantly reduced. We publish the floating margin rate list monthly, which requires stakeholders to update their records, and systems every month. These monthly margin rate changes are typically small percentage changes that occur below the proposed floor margin rates during prolonged periods of low market volatility.

No technological implications are expected as a result of the Proposed Amendments. After we receive approval from our Recognizing Regulators, we intend to implement the Proposed Amendments within 90 days.

Upon implementation we plan to:

The Proposed Amendments would:

IIROC’s Board of Directors (Board) has determined the Proposed Amendments to be in the public interest and on March 23, 2022 approved them for public comment.

The Proposed Amendments were developed in consultation with the FOAS Capital Formula Subcommittee.

After considering the comments on the Proposed Amendments received in response to this Request for Comments together with any comments of the Recognizing Regulators, IIROC may recommend that revisions be made to the applicable Proposed Amendments. If the revisions and comments received are not of a material nature, the Board has authorized the President to approve the revisions on behalf of IIROC and the proposed amendments as revised will be subject to approval by the Recognizing Regulators. If the revisions or comments are material, the proposed amendments including any revisions will be submitted to the Board for approval for republication or implementation as applicable.

Appendix A – Blackline copy of Proposed Amendments to IIROC Rules

Appendix B – Blackline copy of Proposed Amendments to Form 1

Appendix C – Clean copy of Proposed Amendments to IIROC Rules

Appendix D – Clean copy of Proposed Amendments to Form 1

Appendix E – List of Canadian and U.S. qualifying indices

Appendix C

Investment Industry Regulatory Organization of Canada

Proposed amendments to the IIROC Rules and to Form 1 regarding the floating index margin rate methodology

Clean copy of the proposed amendments to the IIROC Rules

Amendment #1 – IIROC Rule subsection 5130(4) is amended to replace the term “major broadly based index” with “major widely quoted market index” as follow:

| “foreign listed equity securities eligible for margin” | Securities (other than bonds, debentures, rights and warrants) listed on an acceptable exchange outside of Canada and the United States that are constituent securities for the exchange’s major widely quoted market index, and the index is on IIROC’s list of foreign market indices whose constituent securities are eligible for margin. |

Amendment #2 – IIROC Rule subsection 5130(9) is amended by:

in alphabetical sequence:

| “broad based index” | An equity index in which:

|

…

| “cumulative relative weight percentage” | An overall relative weight percentage determined by calculating, in accordance with subsection 5360(7), the actual basket weighting for each security in a qualifying basket of index securities in relation to its latest published relative weighting in the index. |

…

| “floating margin rate” | The floating margin rate set by IIROC in accordance with subsection 5360(5), subject to the minimum floor margin rate in subsection 5360(2). |

| “incremental basket margin rate” | The incremental basket rate for a qualifying basket of index securities calculated in accordance with subsection 5360(8). |

…

| “index” | Either a broad based index or a sector index. |

…

| “qualifying basket of index securities” | A basket of equity securities with the characteristics in subsection 5360(6). |

…

| “regulatory margin interval” | IIROC’s regulatory margin calculation determined in accordance with subsection 5360(4). |

| “sector index” | An equity index in which:

|

…

| “tracking error margin rate” | The last calculated regulatory margin interval for the tracking error resulting from a particular offset strategy, subject to the minimum floor margin rate in subsection 5360(2). |

Amendment #3 – IIROC Rule subsection 5360(1) is amended by adding references to both the “greater of” and minimum floor margin rates in the margin calculations, as follows:

5360. Index participation units and qualifying baskets of index securities

The minimum Dealer Member inventory margin and client account margin requirements for index participation units and qualifying baskets of index securities are as follows:

Minimum margin required | |

|---|---|

Category (i) | Category (ii) |

multiplied by

|

multiplied by

|

Amendment #4 – IIROC Rule section 5360 is amended by adding new subsection 5360(2) as follows:

The minimum floor Dealer Member inventory margin and client account margin rates for the purposes of subsection 5360(1) and offset strategies recognized in Rule 5700 are as follows:

| Qualifying index, individual and offset strategies | Category (i) | Category (ii) |

|---|---|---|

| Floor rate percentage to be used in determining margin rate for unhedged positions in index participation units and qualifying basket of index securities | 10.00% | 15.00% |

| Floor rate percentage to be used in determining tracking error margin rate for qualifying offset strategies involving index products | 2.00% | 3.00% |

Amendment #5 – IIROC Rule section 5360 is amended by adding new subsection 5360(3) as follows:

Amendment #6 – IIROC Rule subsection 5360(2) is amended by renumbering to subsection 5360(4) and adding clause 5360(4)(ii) as follows:

IIROC calculates a regulatory margin interval according to the following formula:

|

| 3 (for a 99% confidence interval) |

| Square root of 2 (for 2 days price risk coverage) |

| rounded up to the next ¼%. | ||||

| ||||

Amendment #7 – IIROC Rule subsection 5360(3) is amended by:

as follows:

Amendment #8 – IIROC Rule subsections 5360(4) through 5360(6) are amended by renumbering sequentially and updating the references in clause 5360(7)(ii), as follows:

The incremental basket margin rate for a qualifying basket of index securities is calculated as the sum:

| Market value of each underweighted security in basket | x | Margin rate for that security | x | The % by which the security is underweighted (calculated according to the formula: published relative weighting of the security - actual basket weighting of the security) |

for each underweighted security in the basket.

Appendix D

Investment Industry Regulatory Organization of Canada

Proposed amendments to the IIROC Rules and to Form 1 regarding the floating index margin rate methodology

Clean copy of the proposed amendments to Form 1

Amendment #1 – Form 1 (general notes and definitions) is amended by updating the term “broad based index” to mirror the proposed amendments to the term in subsection 5130(9), as follows:

| “broad based index” | An equity index in which:

|

04/28/22

22-0063

Welcome to CIRO.ca!

You can find the Canadian Investment Regulatory Organization (CIRO) at CIRO.ca with our fresh look and feel.